When Penny-Pinching Backfires: How Insurance “Savings” Cost $54k a Year

What happens when an insurance company denies a cheap medication, only to approve a drastically more expensive alternative? Reddit’s r/MaliciousCompliance community found out in spectacular fashion, thanks to one user’s epic tale of bureaucratic blunders and corporate “logic” run amok. Spoiler: the insurance company’s attempt to save a few bucks ended up costing them tens of thousands more—and the internet had thoughts.

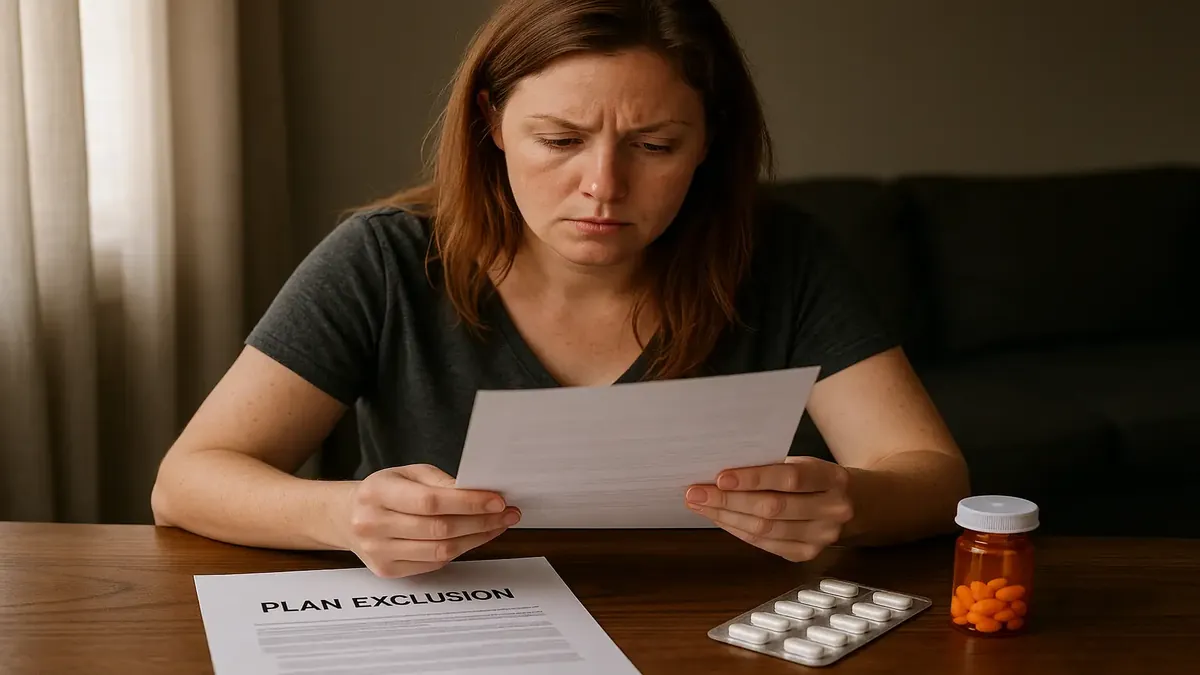

The $900 Medicine That Became a $54,000 Problem

Our story’s protagonist, u/LeathalBeauty, has a long history with a certain insurance company and a unique medical need: due to absorption issues, only liquid, sublingual, or IV medications work for them. For years, their thyroid medication (liquid form) was covered—until the new plan year. Suddenly, insurance denied coverage, leaving the OP to either pay $75/month out of pocket or fight the system.

After a marathon of phone calls and a patient advocate’s intervention, they discovered something wild: while the affordable liquid thyroid med was excluded, the plan enthusiastically covered the IV version—no prior authorization, no step therapy, no questions. The catch? The IV drug costs the insurance company $4,500 per month. That’s $54,000 a year for a medication the patient previously got for $900 annually.

As OP put it, “Corporate stupidity at its finest… No wonder medical care in America costs so much!”

Reddit Reacts: Malicious Compliance, Corporate Facepalms, and Luigis Everywhere

The r/MaliciousCompliance crowd was delighted by this tale of “penny wise, dollar foolish” policy. The top comment from u/Intelligent-Dot-8969 suggested, “You can ask your insurance company to add a medication to their formulary for you. We have had success doing this.” OP agreed—but noted, with a mischievous twist, “figured I’d let them pay for 1 month of the IV medication to help ensure they learn to make better decisions.”

This spirit of fighting back was echoed throughout the thread. As u/Tikki_Taavi quipped, “They figure if they make it a hassle or painful you will stop trying. Old trick.” Only, as OP responded, the insurance company “underestimated who they were playing FAFO with.”

But the madness didn’t stop there. Other commenters stacked up similar stories of shortsighted denials leading to even greater expenses:

- u/Lusankya told of insurance denying a $10k medication, which led to months of disability leave and ultimately cost the company far more.

- u/Choice-Judge-1809 recounted a $90 knee brace denial, only for the insurer to be forced into paying for a $1,400 custom brace (and $5,500 in city overtime costs) instead.

The consensus? These policies often make no fiscal—or medical—sense. As u/Think-notlikedasheep put it: “Penny wise and dollar foolish.” Another user, u/queequagg, expanded on the cold calculus: Insurance companies know most patients will just give up or pay out of pocket, so screwing the few who resist is still profitable. But in rare cases like OP’s, the system’s own logic becomes its undoing.

When the Plan Backfires: Community Insights and Industry Realities

Several commenters with inside knowledge weighed in, offering glimpses behind the insurance curtain. u/Lurkernomoreisay pointed out that many large employers are “self-insured,” and thus have a vested interest in keeping costs low—if only they knew about these gaffes. “Loop in your HR team,” advised u/Mira_DFalco. “Once they see how much more expensive it is, they may approve shifting you back to the cheaper treatment.”

Others highlighted the disconnect between pharmacy and medical benefits, the perverse incentives to push patients toward inconvenience (or out-of-pocket costs), and the bureaucratic nightmare of modern healthcare. As u/SingapuraKitten, a former doctor’s office worker, shared, “For every case like OP’s, there are many others who simply absorb the costs or stop taking their non-covered medications, and the insurance companies profit.”

And sometimes, as u/LeathalBeauty [OP] clarified, the insurance company “did not anticipate that my doctor would be perfectly comfortable writing for the IV version.” Unlike many, OP had both a savvy doctor and the will to push back—a rare and potent combination.

The Final Twist: When Insurance Eats Crow

Here’s the cherry on top: less than ten days after the insurance company paid the eye-watering bill for the IV medication, they reached out to OP with an offer to cover the original, cheaper medication—provided their doctor would switch the prescription back. As OP slyly noted, now might be the perfect time to revisit other denied claims before making that change.

It’s a mischievous, satisfying end to the saga—and a lesson for anyone caught in the gears of American healthcare: sometimes, compliance is the most malicious thing you can do.

Conclusion: Share Your Own Insurance Facepalms

Have you ever been caught in a web of corporate “logic” that defies common sense? Do you have your own tale of insurance shenanigans, medical billing mysteries, or Kafkaesque customer service? Share your stories in the comments—because sometimes, laughter (and a little malicious compliance) really is the best medicine.

Original Reddit Post: Plan Exclusion... Bet they're going to regret it.